This function computes the Akaike Information Criterion (AIC),

Bayesian Information Criterion (BIC),

and Extended Bayesian Information Criterion (EBIC)

for a given matrix of predictors X, a matrix of outcomes Y,

and a vector of lambda hyperparameters for Lasso regularization.

Arguments

- YStd

Numeric matrix. Matrix of standardized dependent variables (Y).

- XStd

Numeric matrix. Matrix of standardized predictors (X).

XStdshould not include a vector of ones in column one.- lambdas

Numeric vector. Lasso hyperparameter. The regularization strength controlling the sparsity.

- max_iter

Integer. The maximum number of iterations for the coordinate descent algorithm (e.g.,

max_iter = 10000).- tol

Numeric. Convergence tolerance. The algorithm stops when the change in coefficients between iterations is below this tolerance (e.g.,

tol = 1e-5).

Value

List with the following elements:

criteria: Matrix with columns for lambda, AIC, BIC, and EBIC values.

fit: List of matrices containing the estimated autoregressive and cross-regression coefficients for each lambda.

See also

Other Fitting Autoregressive Model Functions:

FitMLVARDynr(),

FitMLVARMplus(),

FitVARDynr(),

FitVARLassoSearch(),

FitVARLasso(),

FitVARMplus(),

FitVAROLS(),

LambdaSeq(),

ModelVARP1Dynr(),

ModelVARP2Dynr(),

OrigScale(),

PBootVARExoLasso(),

PBootVARExoOLS(),

PBootVARLasso(),

PBootVAROLS(),

RBootVARExoLasso(),

RBootVARExoOLS(),

RBootVARLasso(),

RBootVAROLS(),

StdMat()

Examples

YStd <- StdMat(dat_p2_yx$Y)

XStd <- StdMat(dat_p2_yx$X[, -1])

lambdas <- 10^seq(-5, 5, length.out = 100)

search <- SearchVARLasso(YStd = YStd, XStd = XStd, lambdas = lambdas,

max_iter = 10000, tol = 1e-5)

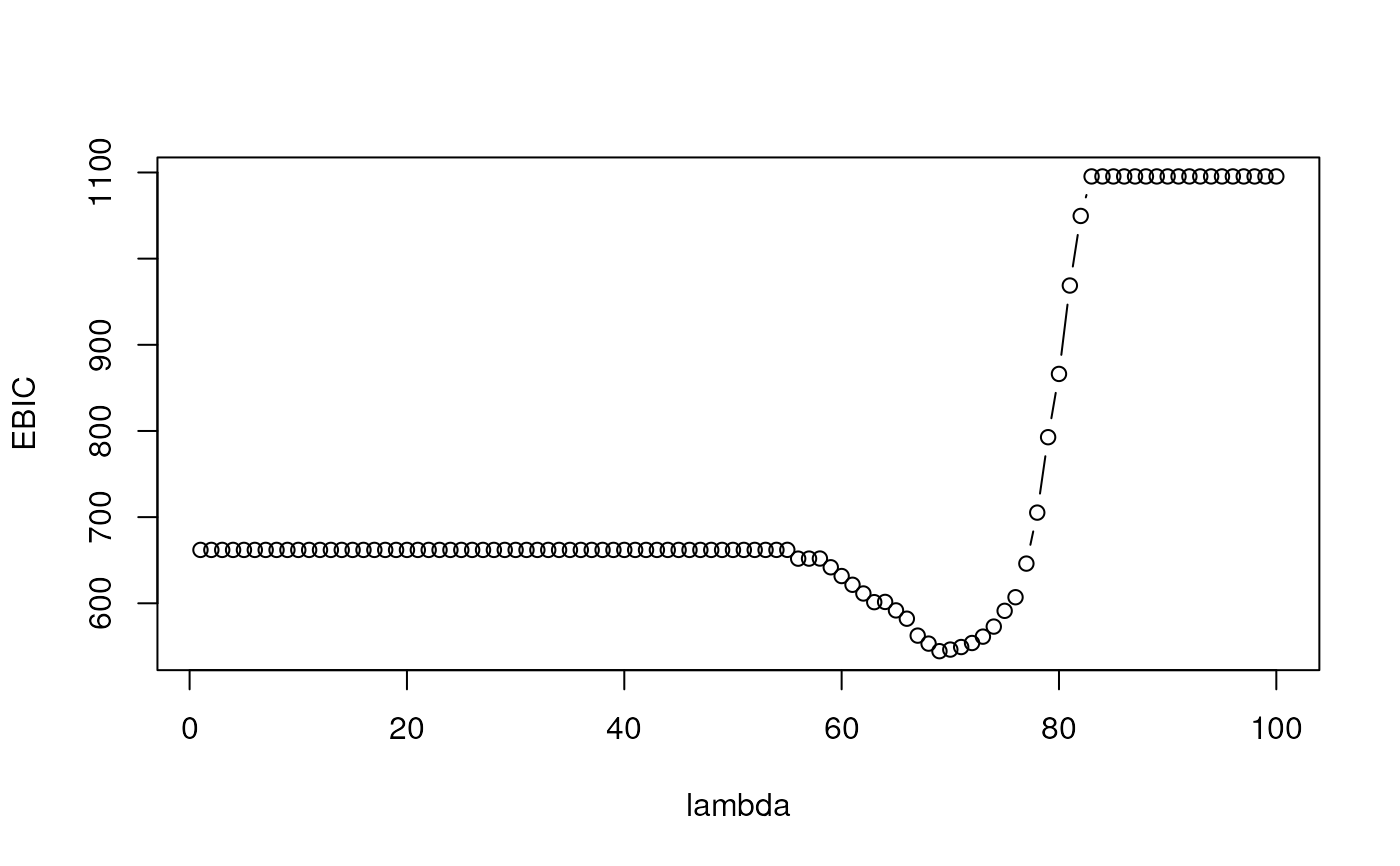

plot(x = 1:nrow(search$criteria), y = search$criteria[, 4],

type = "b", xlab = "lambda", ylab = "EBIC")